Driving Change – Better Services

Posted: Thu 30 November, 2023 Filed under: Business, Cazoo, Customer Services, Domestic, Getting Organised, Insurance, Thoughts 1 Comment »Following on from the utter farce with Cazoo being shockingly shit at customer services, it’s only fair to mention that there have been other companies who have made things a lot easier than they could have been.

First among those has been Enterprise, who have always been a stand-out for me when it comes to car-hire firms. They have one simple thing that makes them stand out (and I don’t understand why other hire firms don’t mimic it) in that quite simply, they come to collect you rather than insisting on getting to them. Alongside that, there’s been no hassle when I’ve needed to extend the hire period and so on. I know that really it’s “just” a case of doing the jobs they’re paid to do, but sometimes even that feels like a rarity.

Honourable mention also goes to We Buy Any Car, who again just did what they said they would – I got the old Kia to them, they checked it out (and explained the entire process really clearly) and paid what they’d agreed within the day. All the paperwork came through fine, the V5C change of ownership and so on, and it was all smooth and easy. (Cazoo wouldn’t do a trade-in on the Kia, as it was over their mileage limit, which is fair enough)

Alongside that, even my car insurers (Darwin Insurance) made life easy. Once I’d taken delivery of the car, I checked other insurance providers so I’d got a good idea of costs, and then called my current insurer to see what the charges would be with them. It turned out that sticking with Darwin would mean a premium that was about 50% higher than a different provider, so it made sense to cancel the current policy and start a new one for the new car. Darwin made that cancellation process easy and smooth – and it turned out that I’d paid enough that I got a refund rather than having to pay the cancellation fee. (Which has just *got* to be a win!) The new policy has also all come through fine and been easy to sort.

So, despite Cazoo being a monumental pain in the arse, there’ve been others who’ve made the entire thing a lot easier than it could have been. And that’s something I’m deeply thankful for.

Unhelpful Timings

Posted: Tue 7 November, 2023 Filed under: Domestic, Finances, Insurance, KwikFit, Thoughts 2 Comments »The one downside of the whole “need a new car” thing is that I’d only recently sorted out all the MOT, Servicing, Tax, and Insurance Renewal for the current car. Which is, to say the least, a bit annoying.

Thankfully, the MoT hadn’t needed too much work – simply realigning windscreen wipers and headlamps, no major stuff at all – but still it’s annoying to have done all the stuff for ensuring it’s mechanically OK, only to then have something unchecked go ker-fut. (OK, *start* to go ker-fut!)

The insurance renewal is a bit more of a pain. I could make alterations, but I suspect that the massive difference in vehicle values might make it ridiculous. So I might have to cancel the newly-renewed policy – I know what that will cost, and it’s doable. And before I make a decision, I’ll find out what the costs will be, so I can properly evaluate the pros and cons.

Again, things could be far, far worse. It’s just annoying.

Excessive Renewal

Posted: Thu 25 February, 2021 Filed under: Customer Services, Domestic, Finances, Insurance, Lockdown, Travel Leave a comment »This time last year, I was planning on going to a friend’s wedding over in Madeira, and bought some travel insurance along the way.

Obviously it didn’t work out, because of Covid and the like, and the insurance didn’t get used for any other trips, for similar reasons. Thankfully, I’d had a good deal on it, so wasn’t too upset. Them’s the breaks, and all that.

This week, I got the renewal letter from the company, telling me what I’d pay this year.

Now OK, there’s been a lot going on in the world this year, and I assume insurance has taken a kicking (although I wouldn’t have thought it was a huge one, in comparison to travel companies, credit cards and the like) but still, the increase from last year to this is a 50% rise. And bear in mind, there’s no way I’d be using it ’til at least May/June, so it would cost me more to able to use it for less time.

Needless to say, they’ve been told to fuck off. I’ll buy travel insurance again as and when I need it – but that’s still not going to be any time soon.

Reinsuring

Posted: Wed 25 September, 2019 Filed under: Advertising, Brands, Change, Customer Services, Cynicism, Domestic, Driving, Finances, I Don't Understand, Insurance, People, Weirdness Leave a comment »The world of Car Insurance is very, very strange. I truly don’t understand how it all works.

My car insurance is due for renewal in October, so I recently received the renewal gubbins from my current insurer. They’ve put my insurance up by £60 for the year. Bear in mind, I’ve not even spoken to them all year, let alone made a claim, and I’ve now got another year’s no claims discount as well. And yet it’s gone up.

So I shopped around, doing the usual comparison website thing (Meerkats rather than opera singers) and got one that’s actually £120 cheaper than what I was being offered by the current insurer – and with slightly better cover.

Brilliant, I’ll sign up and do that. Job done. And this is where it all gets weird(er)

My new insurer is actually one I used a couple of years ago. So when I log in to their ‘self-service portal’ to see my new policy, all I can see is the details of the old one. Fuck sake. (It looks like the policy is actually tied to a combination of my username and password – so I can change password, and now view the new details instead – but I didn’t know that at the time)

So first things first, I call my current insurer to tell them I won’t be renewing with them. It’s the usual automatic phone gubbins, and gives the name of the insurance provider – let’s call them ABC Insurers, for the sake of argument. I give the correct information, go through, tell them I won’t be renewing, explain why, and it’s as easy as that.

Then I call the new insurers. Who are also using ABC Insurers. So I go through the correct information for the new insurance, get things sorted, get the documents emailed to me, and it’s as easy as that.

But it’s weird – I’ve used two different companies (well, two different front-ends) and given them the same information (obviously) but one faction is offering me a significantly better deal than both the one I’m on, and the renewal quote from the one I’m on. But they’re both the same company underneath!

How the fuck does that make sense? Offering the same person two completely different prices (and slightly different packages/benefits) Why not allow my current insurer to offer the same price as my new one? It’s all just a bit bizarre.

Re-covered

Posted: Fri 29 September, 2017 Filed under: Advertising, Customer Services, Cynicism, Domestic, Driving, Insurance, Loyalty Schemes, Thoughts 4 Comments »Somehow, it’s already nearly a year since I got the latest car. Which, of course, means it’s also time for my insurance renewal to come through.

As usual, the current company have massively taken the piss, nearly doubling my premium this time round. For some reason, rather than having a number of different under-writers, they’ve recently decided to stick with just the one – and that one happens to be nothing short of extortionate.

Still, that’s fine, they can fuck off.

As a result, I’ve already sorted out a new policy with a different company. It’s got all the cover and options I wanted, and is cheaper than what I’ve paid this year, let alone the ridiculous renewal price.

I truly don’t understand the business model of the insurance industry, this attitude of “keep on charging more ’til people leave”. Surely if someone’s been with a company for [x] years, and established a record of being safe, not claiming etc., then it should be easier/cheaper/better to keep them, rather than letting them sod off somewhere else?

I suppose it might be the law of diminshing returns, an expectation the customers will claim eventually. Using that it kind-of makes sense, if all the customers are paying up, and if we can get rid of them before they cost us, then we’ve made money out of it, and it’s cost “some other company”.

But it all seems pretty flawed to me, and pretty bloody dumb. Hey ho. Their loss, not mine.

Long Week

Posted: Fri 13 May, 2016 Filed under: Car Repairs, Customer Services, Domestic, Driving, Getting Organised, Insurance, M1, Travel 1 Comment »So far, it’s felt like a very long – and really quite unproductive – week in many ways.

I was away over the weekend, and while driving back on Sunday, the car died on me near Leeds. No power-steering, idiot-lights galore – and all while travelling at 80-ish in the outside lane of the M1. That definitely focusses the mind somewhat.

I got over to the hard shoulder immediately, and stopped. Called my insurance company – who also do the recovery part – and got it organised. I knew it was 99.9% likely to need recovery, so they sorted it out and that all went really smoothly. They’d predicted up to 90 minutes before the recovery got there, and they turned up within half an hour.

Apparently, I got lucky – my recovery part includes “Get me home”, rather than the more standard “nearest garage, and then pay through the nose for anything else” policy. So I got one truck that took me back to Milton Keynes in one go (no Relay crap either, thankfully) and dropped the car off at the Saab garage locally, and then I got a cab home. Not cheap, but could’ve been so much worse. According to the recovery driver, if it’d been the normal policy, it would’ve cost me around £500 to get the car home… I broke down at 1.30, and was back in Milton Keynes at 6.00, and home by 7.00. Not at all bad, all things considered.

While I was waiting to be picked up, I’d also organised a replacement hire car – which also reminds me yet again how great smartphones and apps can be, sat by the side of a motorway booking a hire car – that I collected on Monday before heading off to Chesham to be on-site again. All fine. Hassle-filled, but fine.

After doing a bundle of driving and so on, I got home about 9pm, and parked up.

And on the Tuesday, by 7am the battery was completely flat and the hire car wouldn’t start at all. Cue a three-hour farce with the AA not sending anyone when they said they would, and making an utter bollock of the entire process. Not helped by using the hire-firm as an intermediary (although they handled it fine, it was just the AA being useless) but still. I finally got sorted at mid-day.

So yes, it took the AA three hours to find a known address and fix the problem (Epically flat battery, although we don’t yet know why – apparently Fiat couldn’t find any issues with it) where it only took four-and-a-half for another company to find me on a motorway, and drive 180-ish miles. Safe to say, I won’t be putting any money in the AA’s direction any time soon.

Along the way, the Saab was fixed on the Monday – the power-steering belt, which also powers a number of other bits, had snapped, and it was just that part which required replacement. So, a bill of £85 all-in, including VAT, labour and parts. Could’ve been *so* much worse…

The rest of the week has just been busy and ridiculous, and doesn’t really feel like it’s stopped at all. With luck it’ll ease up now for the weekend – but then, this is me, so what’re the chances? Low-to-sod-all , I’d say…

Ker-Fut 2 – Getting to the Garage

Posted: Mon 6 July, 2015 Filed under: 1BEM, Car Repairs, Customer Services, Domestic, Driving, Getting Organised, Insurance, Milton Keynes, People Leave a comment »F0llowing on from Friday’s car issues, it’s been a semi-eventful weekend.

When I got home on Friday, my first job was sorting out a hire car for the coming week (possibly two) as I’m all over the place. That got sorted relatively easily – one place was closed, and I’d have had to call their Glasgow office to try and find out what was available (a ridiculous state of affairs, and frankly, fuck that) and the second one, while closed, enabled me to book a car to be collected the following morning, in a dead easy process.

And then it was a small case of hunting for the necessary identity documents. Driving licence (and the new necessary code from DVLA for the online driving record – needed since the paper part of the licence is now outdated) was OK, as was passport – but finding documents to prove address were somewhat more difficult, as I now do all my bills online, so rarely get anything “official” through the post. (As an aside, I wonder how that will change things over the next couple of years, as more and more paper-based stuff is removed/reduced/made into a cost) I did find the necessary bits in the end, but it’s getting to be more hassle than it should be.

Collecting the car (a new Vauxhall Insignia, which is not at all bad, as Vauxhall’s go) was an absolute doddle. The place is quite new, but was really a case of walk in, do the paperwork, check the car, bugger off. All told it was less than 30 minutes – fairly impressive. Because I’d used the same company before (when the Mondeo died on me) I had a lot less ID-checking to do – which seemed odd, as that was two-and-a-half years ago, and lots could’ve changed since then – but it was a nicely painless experience all round.

I’ve plonked about with it a fair bit over the weekend, and yeah, not bad at all.

I’ve also been looking at replacement vehicles – I suspect the Saab has blown up significantly, and will be more to repair than it’s worth, so I’m sounding out alternatives – and there’s a couple I’m going to check out this week, once I know more about the state of the Saab.

And then we come to getting the Saab to the garage. I’d thought a lot about this, and decided that the best plan would be to drive it (slowly, and along backroads) to the garage on Sunday, avoiding all the heavy traffic and any potential issues. If it died, well, I’ve got recovery as part of my car insurance. I left it ’til later in the Sunday, rather than trying to do it while people were still going shopping and so on. I did have my doubts about the plan – but figured it was infinitely better than trying to do it on Monday evening, let alone Tuesday morning!

Anyway, set off lateish on Sunday afternoon (about 5.30) and it was all fairly successful. I got most of the way fine, but then it did die out properly, so I had to do the recovery thing. In fairness, even that ended up going really smoothly – the recovery vehicle turned up within half an hour, and took me to drop the car off at the garage. (I was actually really lucky, because one thing I hadn’t taken into consideration was the fact it was the Grand Prix at Silverstone, so traffic and breakdowns were greatly increased later on!)

Then it was just a case of dropping off the keys, and getting a cab home – all told, I was home by 8pm, which wasn’t bad, when everything was taken into consideration.

Replacement Glass

Posted: Wed 21 August, 2013 Filed under: Customer Services, Domestic, Driving, Insurance 8 Comments »Last week, when I was driving over for the interview in Cambridge, the windscreen got hit by a stone thrown up by the car in front. It chipped the windscreen pretty seriously, although it didn’t crack or break. It’s been annoying me since – it was right in my viewline – but I didn’t have a chance to get it repaired ’til today, due to doing lots more driving and commuting to office etc.

Getting hit by a stone like that is quite a sobering experience – or at least it is if you think about it a bit. You realise just how piss-poor your reaction time truly is. OK, it’s a closing speed of 140mph-ish (stone coming towards me propelled (I assume) at 70mph-ish from a vehicle travelling at that speed, towards a car travelling towards it at 70mph) but still, you see a blink of something coming towards you – indeed, in this case directly at you – and then the impact. You haven’t even had time to flinch. I assume that when it’s bigger items (you know, a car coming towards you, for example) you’ve had a bit more warning, a bit more time to prepare, but I don’t know. Honestly, I hope I never find out.

Anyway, this glass repair had to be organised through the insurance company this time, rather than the age-old technique of finding a company doing it in supermarket carparks. (It turns out that this used to be fine, but then became a nightmare of companies doing the same, invoicing insurance companies, and generally just all going to cock. Now the industry has entered the world of approved/preferred suppliers, organised through third parties etc. etc.) So all arranged for today.

They’ve tried to just repair the chip, but that hasn’t taken, for whatever reason. (Personally I think Saab glass has some weird coating on it that doesn’t like rubber suction cups. I know my SatNav has always had problems sticking to the glass, and on this occasion the equipment in use with suction cups was also failing to stick.)

So now I’m getting a full replacement windscreen. Bit of a pain in the tits, but at the same time I know there were other (far smaller) chips, so at least with a new screen it’s clean of issues and damage. I suspect it’ll be weird for a couple of days, having a completely clean screen. It won’t last…

Phone Insurance – You couldn’t make this shit up

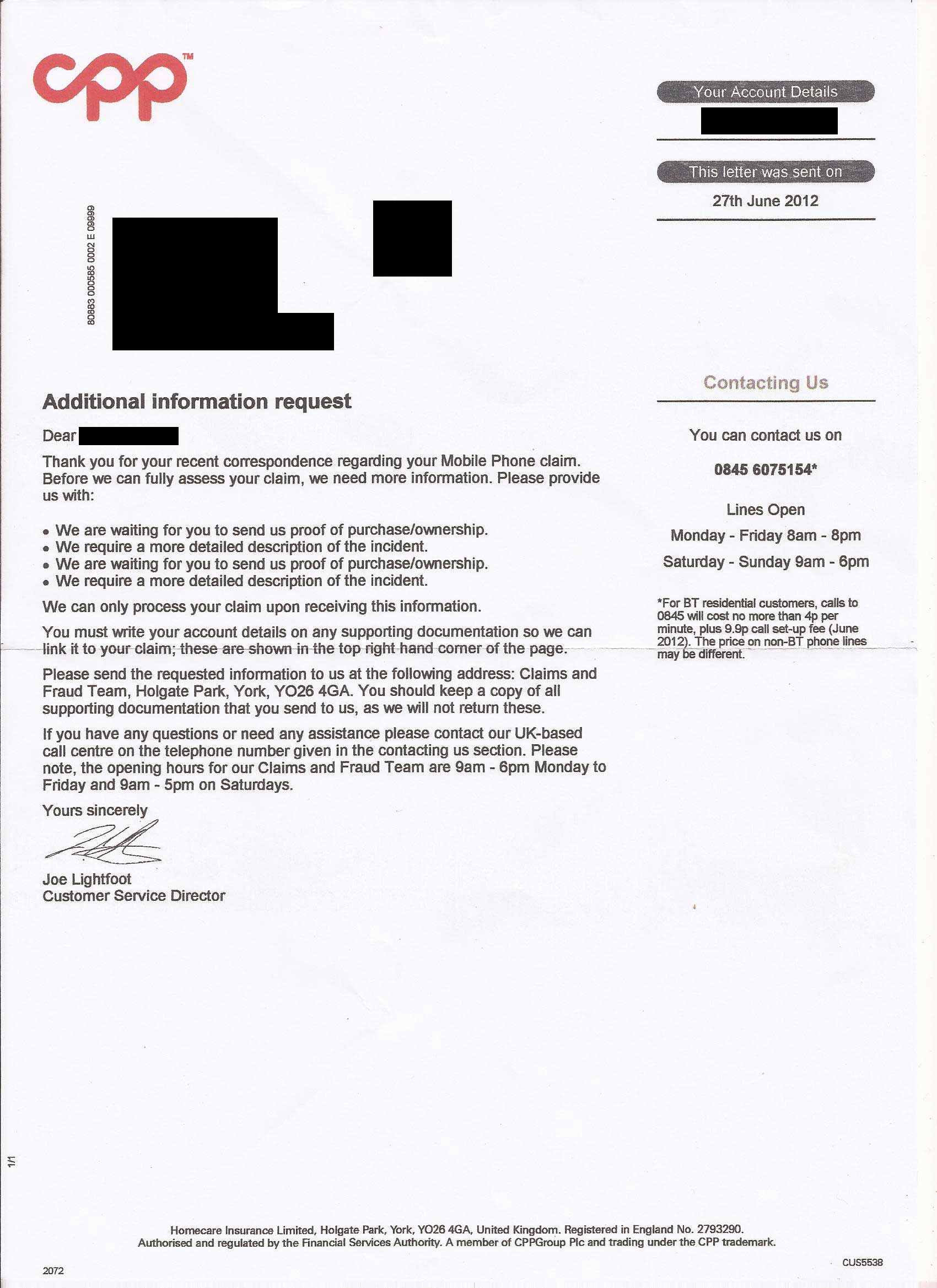

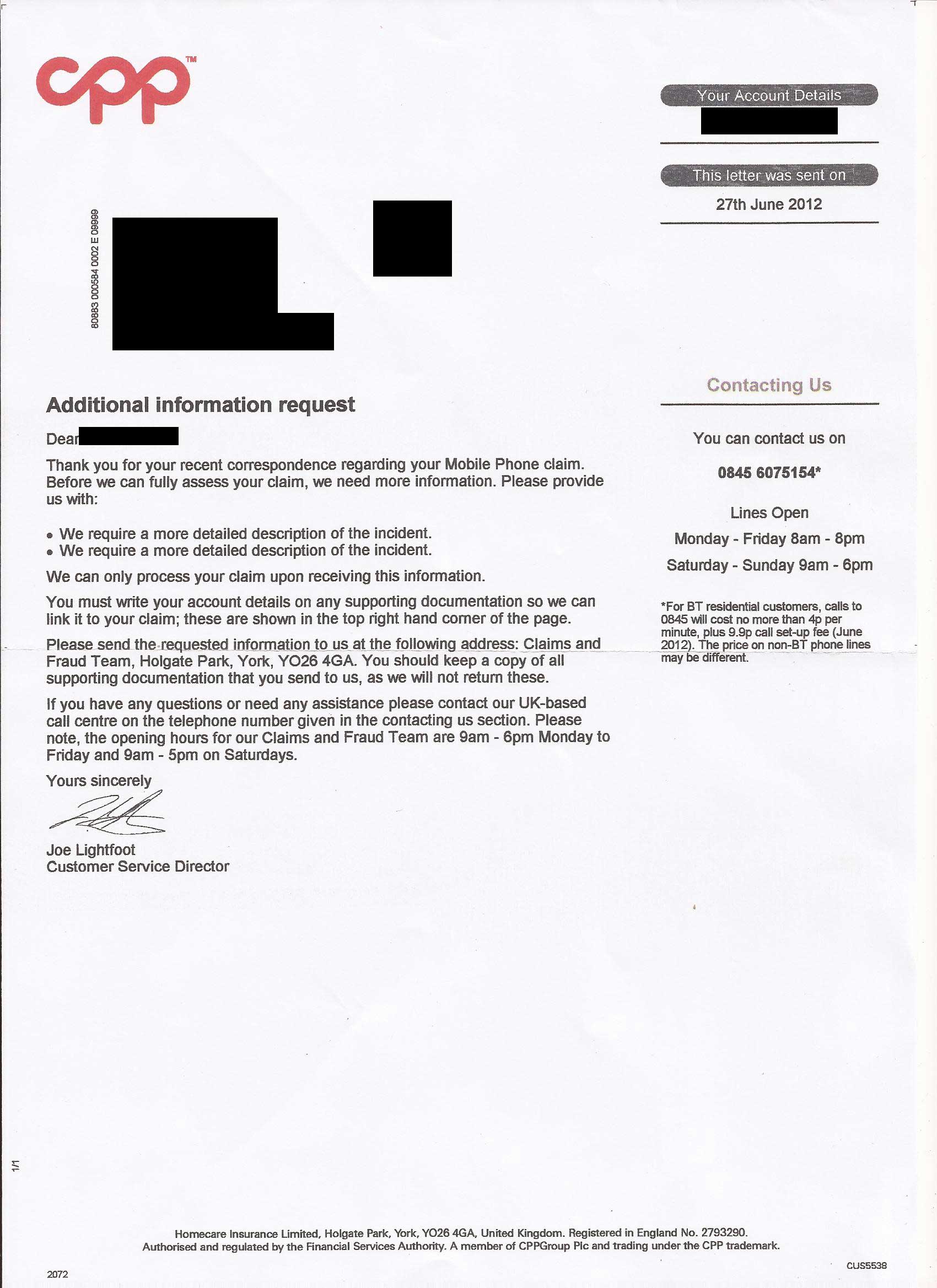

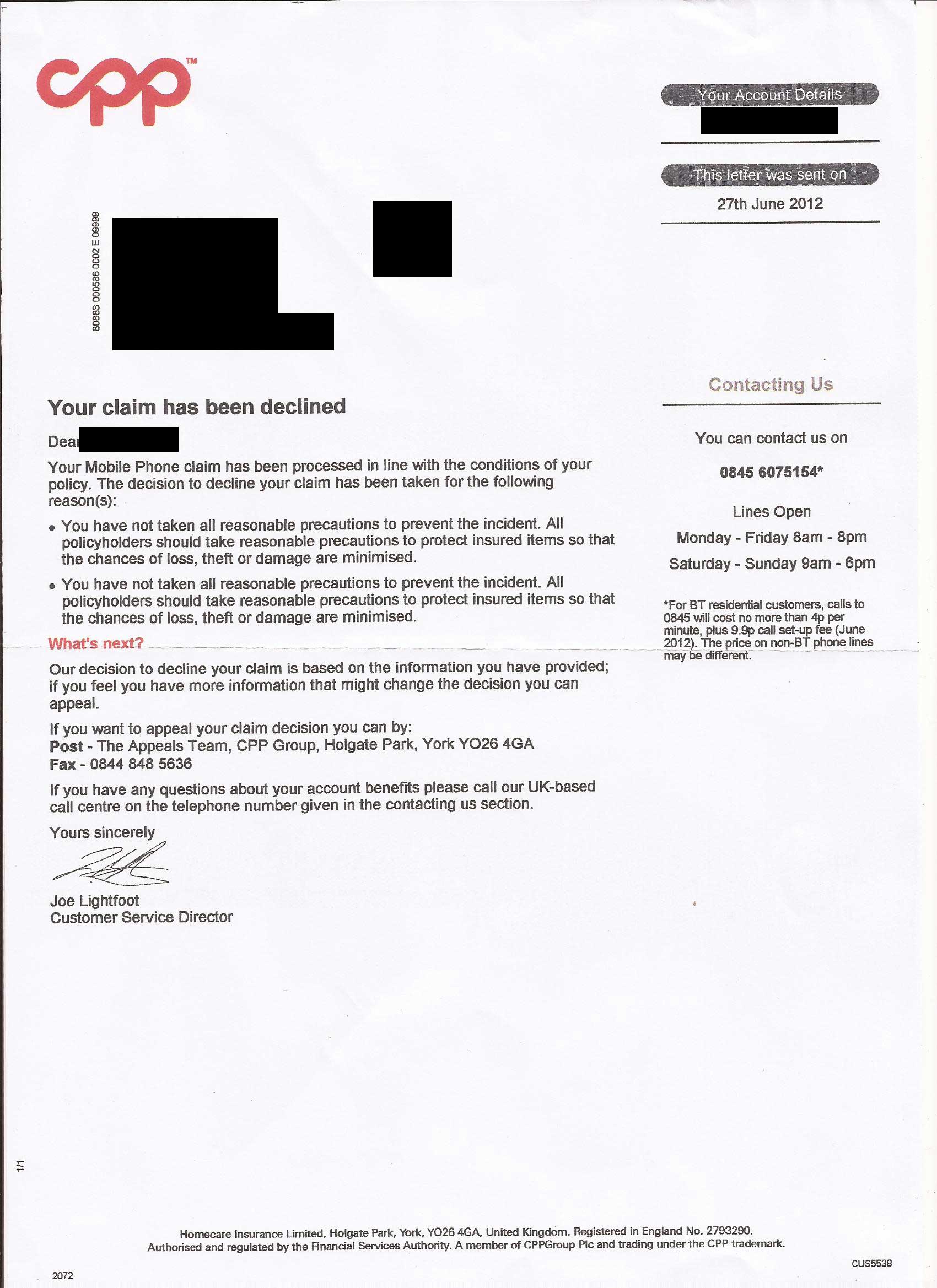

Posted: Mon 9 July, 2012 Filed under: 1BEM, Customer Services, Cynicism, Insurance, iPhone 2 Comments »This morning, I got three letters from CPP, the muppets company dealing with the claim for my knackered iPhone.

All three are dated the same day – 27th June! Nearly two weeks to get sent out – and all ‘signed’ by the same person. Combined, they make for a brilliant record of how CPP handle things. Well, it’s hilarious if you’re not receiving them.

- Letter 1 – “We need more information – proof of purchase, and a more detailed description of what happened”

- Letter 2 – “We need a more detailed description of what happened” – guess this means they’ve received the proof of purchase ?

- Letter 3 – “Claim denied”. So they’ve received a more detailed description? Or did the one in the initial phone call suddenly suffice?

{kind=link}

{kind=link}

{kind=link}

And bear in mind, this is all two weeks ago – it’s already been appealed, and complained about.

I wonder what excuse they’ll use for these letters, and the fact it’s taken two weeks to receive them…

Phone Insurance – Rejected

Posted: Thu 28 June, 2012 Filed under: 1BEM, Charm School, Customer Services, Cynicism, Domestic, Insurance, Stupidity 6 Comments »So, following on from yesterday’s post about the idiots at Homecare Insurance (part of CPP Insurance) it now turns out they’ve rejected my claim, because I “didn’t take reasonable precautions”.

Now, the phone is (supposedly) covered against accidental damage. But that apparently doesn’t include accidents. Of course, with insurance, the devil is in the details.

The actual circumstances of the phone’s demise are that I left it on the cistern of the toilet while I had a shower. While in the shower, I assume I received a call or a message and vibrated, because the poxy thing was in the toilet when I got out of the shower. And since then, it’s been knackered, for obvious reasons.

So apparently, I didn’t take enough care of the phone. Sure, I could have been in the bathroom, then left, put the phone somewhere else, and gone back in. I could have put the phone somewhere else in the bathroom – a windowsill, or whatever. But the fact is, I didn’t, I didn’t even think past “It’ll be fine on a flat surface”. Which it has been in the past. I didn’t think it’d fall in, because it was on a flat safe surface, not even close to the edge.

And this all means I didn’t (currently) take reasonable precautions. I freely admit to being an idiot, but the process wasn’t a careless or slapdash one – just a stupid one.

It’s being appealed, and the entire process is now also a full formal complaint.

But short story? If you’re insured with Homecare or CPP, don’t expect accidental damage to be covered, even when they say it is.

Missing the Point – Insurance

Posted: Wed 27 June, 2012 Filed under: 1BEM, Customer Services, Cynicism, Domestic, Insurance, Stupidity, Thoughts 1 Comment »Just under two weeks ago, I buggered up my iPhone. Like an idiot, I’d laid it on the cistern of the loo while I had a shower. I assume it received a message while I was showering, vibrated, slid off the cistern, splosh.

Fortunately, the phone is/was insured, so a claim is being processed.Equally fortunately, the insurance is an added benefit to my bank account – and that’s fortunate, because if I was paying for this policy, I’d be a lot more annoyed than I currently am.

The company, Homecare insurance, are part of the CPPGroup and are – frankly – a bunch of clowns.

When I first called, their systems were unavailable. So they said they’d call me back – except they can only call me back on my registered number. Which is, of course, my mobile. Which is knackered, hence why I’m calling them. But you can’t change the number, it’s only the registered one. And when I asked to speak to a manager, they couldn’t be put through because the systems were down. (Why managers are unavailable when the system is down is something we’ll just ignore for now. I suspect it’d make my brain hurt)

So. They can send out a claim form, but you can’t email or fax it back – it’s got to be posted. And then it takes five days to process. Bearing in mind that everything in the policy says “covered against accidental damage, water damage etc.”, I don’t quite know how it takes five days to make that decision.

Anyway. I got an email from the cretins today.

“We have attempted to contact you by telephone to discuss the claim you have made on your phone insurance policy but were unsuccessful in contacting you.“

Yes, they’ve tried calling the mobile number – again – and can’t get through. Considering it’s the phone I’m claiming for, I wonder why they can’t get through?